While the world can count dozens of important currencies, when it comes to top line financial and investment discussions, the currency marketplace really comes down to a one-on-one cage match between the two top contenders: the U.S. Dollar and the Euro.

In recent years the contest has become a blowout, with the Dollar pummeling the Euro into apparent submission. Based on the turmoil created by the European Debt Crisis and the continuing problems in Greece and other overly indebted southern tier European economies, many investors may have come to assume that Euro boosters will be forced to ultimately throw in the towel and call off the entire experiment, thereby leaving the Dollar completely unchallenged as the champion currency, now and for the foreseeable future. This is a stunning turnaround for a currency that was seen just a few years ago as a credible threat to supplant the dollar as the world’s reserve.

Putting aside the fact that there are many important currency relationships besides the euro/dollar axis, economists, journalists, and investors have forgotten the 16-year history of the Euro and how the currency has survived and prospered after many had assumed it might be consigned to the dustbin of history.

The Euro was created in 1992 by the Maastricht Treaty (which created the European Union) but did not come into being as an accounting unit (not a physical currency) until January of 1999. In the lead up to its launch, many had argued that the Euro would become the heir to the rock solid Deutsche Mark, the German currency that had risen to preeminence on the back of Germany’s post war resurgence, high savings rate, enviable trade balance, and post-Soviet unification. With German bankers in a firm leadership position in the European Central Bank and the European Union, many had hoped that the new Euro would adopt the virtues of the Mark. As a result, the Euro debuted with a value of 1.18 dollars. But the honeymoon was short-lived.

Almost immediately from the point it began freely trading the Euro began to encounter severe headwinds. The Russian debt default and the Asian currency crisis in the late 1990’s caused investors to sell assets in the emerging markets and seek safe havens in the dominant economies. This provided a crucial early test for the Euro. But the new currency failed to attract much of this fast flowing transnational investment flow. On the other hand, the U.S. markets and the U.S. Dollar were beckoning as extremely attractive targets.

In the second term of Bill Clinton’s presidency, America, at least on paper, looked very strong. From 1998-2000, based on Bureau of Economic Analysis (BEA) figures, GDP growth averaged 4.4%, which is roughly four times the rate that we have seen since 2008. The expanding economy and the relative spending restraints that had been made by the Clinton Administration and the newly elected Republican Congress resulted in hundreds of billions of annual U.S. government surpluses, the first such black ink in generations. Many economists comically concluded that the surpluses would become permanent (in fact they lasted just a few years). At the same time, U.S. stock markets were notching some of the biggest gains in their history. From the beginning of 1997 to the end of 1999 the Dow Jones surged by approximately 69%. The tech heavy Nasdaq, the epicenter of the “dotcom” bubble, rallied by an eye popping 294%.

As a result, international money began pouring into the Dollar, taking the wind out of the sails of the newly launched Euro. The stretched valuations that had pushed up U.S. stocks to nosebleed levels failed to dissuade investors from piling in well into the mid-point of 2000. Not only had Wall Street spread the gospel of the new economy, where negative earnings and high debt no longer mattered, but many were convinced that the interventionist tendencies of the Alan Greenspan-led Federal Reserve would protect investors against losses.

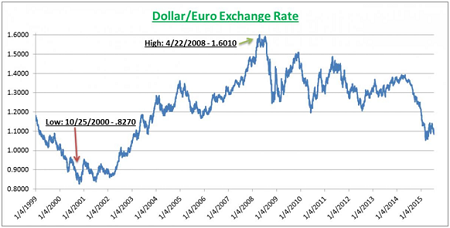

As a result of these forces, the Euro first fell to below parity against the dollar on January 27, 2000 when it closed at 98.9 U.S. cents, a fall of 16% from its debut. After that psychological barrier was breached, the selling intensified. By May 8, 2000 the Euro traded at just 89.5 U.S. cents, an additional 9% decline in just three months. This prompted news stories like a BBC article entitled “Was the Euro a Mistake?” Top economists and investors began wondering if the new currency would last much longer.

The Euro’s reputation was further tarnished in September of 2000 when Danish voters rejected their country’s plans to adopt the Euro. The distaste shown by a small country widely considered squarely in the mainstream of Western European culture was a huge black eye for the Euro experiment. The pessimism sent the currency down another 6% in just one month following the Danish election, reaching what would become an all-time low of just 82.7 U.S. cents on October 25, 2000. At that level the Euro had fallen a full 30% from its debut valuation. It looked like game over. The Euro vs. Dollar was shaping up to be a Bambi vs. Godzilla scenario.

Compiled by Euro Pacific Capital using data from the Federal Reserve Economic Data (FRED) from Federal Reserve Bank (FRB) of St. Louis

When the European debt crisis really started grabbing headlines in 2011, with yields on sovereign debt of the so-called PIIGS nations (Portugal, Italy, Ireland, Greece, and Spain) widening to record territory in comparison to the sovereign bonds of Germany, scrutiny of the Euro came into question once again. The uncertainty over possible bailouts for European banks that were holding potentially toxic government debt was too much uncertainty for the market to handle. The pressure on the Euro was intensified by the slowing Eurozone economy. These forces combined helped to push the Euro down steadily during 2012 and 2013.

Confidence is the only thing that really undergirds modern fiat currencies. But confidence can be very ephemeral…disappearing as quickly as it arrives. The U.S. Dollar benefits from confidence that the Euro currency may just be unworkable, that the U.S. economy will continue to improve, and that the Fed will raise rates throughout the remainder of 2015 and into 2016. If these expectations are unfulfilled, there could be a Euro reversal.

Best Selling author Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital. His podcasts are available on The Peter Schiff Channel on Youtube

Catch Peter’s latest thoughts on the U.S. and International markets in the Euro Pacific Capital Summer 2015 Global Investor Newsletter!