I’m reading a lot of international relations theory, just not blogging that much on it. I’ve been hoping to write a longer entry on the current debate on American decline (see especially Niall Ferguson, at Newsweek, “An Empire at Risk“). But since I just found two real cool posts at TigerHawk on foreign holdings of U.S. treasury securities (here and here), I thought I might as well share with readers an important article I just finished reading. From the Fall issue of International Security, Daniel Drezner, “Bad Debts: Assessing China’s Financial Inluence in Great Power Politics.”

Lots of folks talk about China’s stranglehold on the American economy, that the U.S. is increasingly vulnerable to China’s accumulation of massive currency reserves and treasury holdings. For example, hardline leftist Matthew Yglesias writes, “what we’re seeing on Barack Obama’s Asia trip is that the Bush administration’s squandering of American national power has increased China’s status vis-a-vis the United States.” But as Drezner points out, complex interdependence creates mutual sensitivites, and in fact it’s Washington that enjoys the balance of financial power over Beijing:

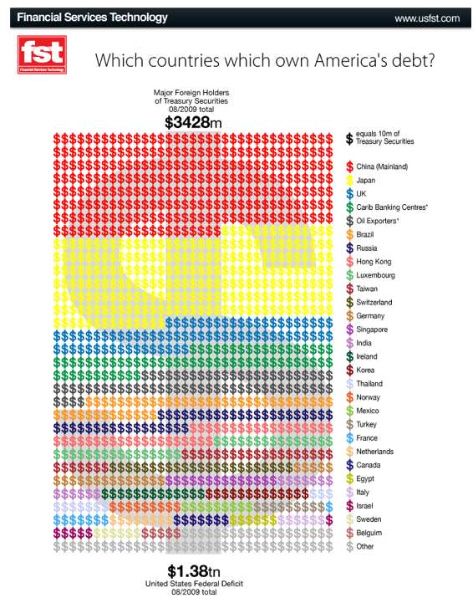

In the wake of the 2008 financial crisis, policy analysts are taking a hard look at the geopolitical implications of the United States’ debtor status vis-Ã -vis its sovereign creditors. America’s ballooning budget deficit and persistent trade deficit have required corresponding inflows of foreign capital. In recent years, official creditors such as central banks, sovereign wealth funds (SWFs), and other state-run investment vehicles have dominated these inflows. The United States owes an increasing amount of money to authoritarian capitalist states. China has risen to special prominence as a creditor to the United States. In September 2008 China displaced Japan as the largest foreign holder of U.S. debt; according to one estimate, Chinese financial institutions owned $1.5 trillion in dollar-denominated debt in March 2009.

What are the security implications of China’s creditor status? If Beijing or another sovereign creditor were to flex its financial muscles, would Washington buckle? Many analysts believe the answer to be yes. In December 2008 James Rickards, an adviser to U.S. Director of National Intelligence Mike McConnell, observed that China possessed “de facto veto power over certain U.S. interest rate and exchange rate decisions.” Similarly, Gao Xiqing, the head of the China Investment Corporation (CIC), recently warned, “[The U.S. economy is] built on the support, the gratuitous support, of a lot of countries. So why don’t you come over and . . . I won’t say kowtow, but at least, be nice to the countries that lend you money.” Whenever sovereign creditors appear to lose their appetite for dollar-denominated assets, it becomes front-page news.

If lending states can convert their financial power into an instrument of statecraft, the implications for the United States would be daunting. As Brad Setser recently concluded, “Political might is often linked to financial might, and a debtor’s capacity to project military power hinges on the support of its creditors.” As the United States continues to run large deficits, many other commentators believe that its power is another bubble that will soon pop.

The use of credit as an instrument of state power in great power politics has received urprisingly little scholarly attention in recent years. Setser observes, “Rising U.S. imports of capital–and the displacement of private funds by state investors–has not produced a comparable literature examining whether state-directed financial flows can be a tool for political power.” A perusal of major security journals reveals no recent discussion of this issue.

This article appraises the ability of creditor states to convert their financial power into political power, drawing from the existing literature on economic statecraft. It concludes that the power of credit between great powers has been exaggerated in policy circles. Amassing capital can empower states in two ways: first, by enhancing their ability to resist pressure from other actors and, second, by increasing their ability to pressure others. As states become creditors, they experience an undeniable increase in their autonomy. Capital accumulation strengthens the ability of creditor states to resist pressure from other actors.

When capital exporters try to use their financial power to compel other powerful actors into policy shifts, however, they run into greater difficulties. As the economic statecraft literature suggests, the ability to coerce is circumscribed. When targeted at small or weak states, financial statecraft can be useful; when targeted at great powers, such coercion rarely works. There are hard limits on the ability of creditors to impose costs on a target government. Expectations of future conflict have a dampening effect on a great power’s willingness to concede. For creditors to acquire the necessary power to exert financial leverage, they must become enmeshed in the fortunes of the debtor state.

More often than not, the attempt to use financial power to exercise political leverage against great powers has failed. Looking at recent history, what is surprising is not the rising power of creditors, but rather how hamstrung they have been in using their financial muscle. To date, China has translated its large capital surplus into minor but not major foreign policy gains. To paraphrase John Maynard Keynes, when the United States owes China tens of billions, that is America’s problem. When it owes trillions, that is China’s problem.

The whole essay is here.

RELATED: Robert J. Lieber, “Falling Upwards: Declinism, The Box Set.”

IMAGE CREDIT: TigerHawk and Computational Legal Studies, “Which Countries Own America’s Debt?“

Cross-posted from America Power.